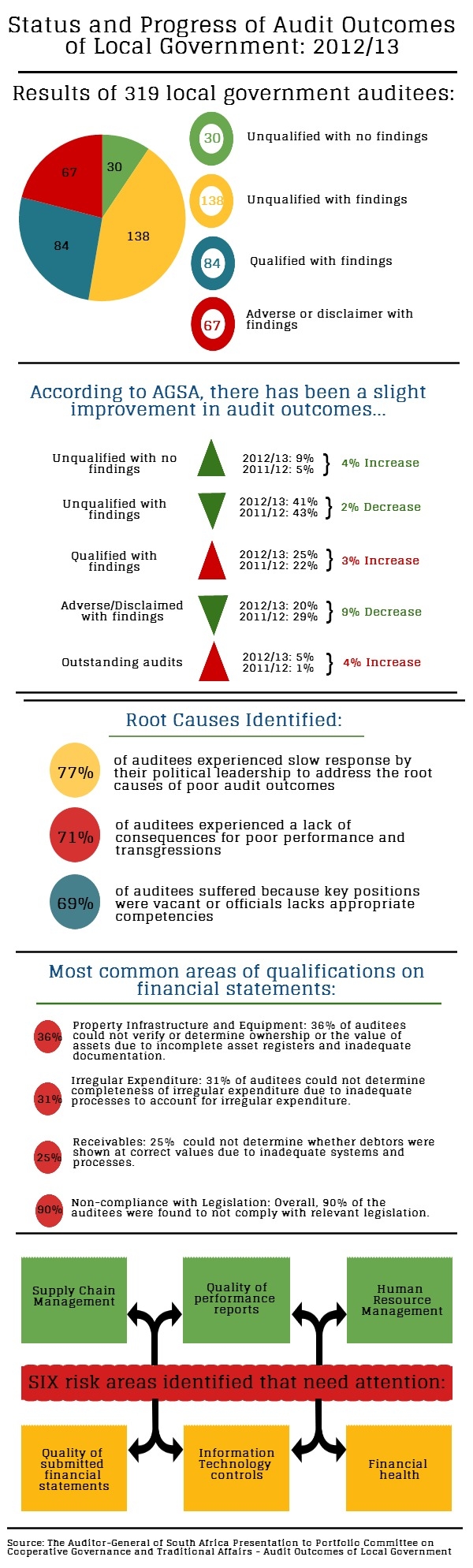

On Tuesday in Parliament, the Auditor-General of South Africa (AGSA) briefed the Cooperative Governance and Traditional Affairs Portfolio Committee on local government audit outcomes for the 2012/13 financial year.

The audit results left Members feeling dissatisfied – while Gauteng, Western Cape and KwaZulu-Natal performed well, the rest of the municipalities in the country remain a concern. Members asked whether municipalities could be said to be improved if they were still spending large amounts of money on consultants to assist them with audits. There were also concerns that 32% of the local government auditees could not pay their creditors within 90 days and that 71% had written off more than 10% of their debt as irrecoverable.

Although financial management at municipal level has been an issue for some time, the AG also pointed out that leadership was a problem. While only three provinces improved, the rest were either stagnant or had regressed due to a high level of non-compliance with procurement regulations, a lack of consequences for transgressions, poor internal controls, and an overall lack of skills in key positions.

See the infographic below for more details, but before you start, here is a breakdown of the technical terms used to describe audit outcomes given by the AG:

Clean audits: When entities produce financial statements without material misstatements; no material non-compliance with laws/regulations; no material findings on performance reports with predetermined objectives that are useful and reliable.

Unqualified opinions with findings: Financial statements are a fair reflection. However, there are findings either on non-compliance with laws/regulations or the performance information is faulty or they relied on auditors to detect and correct errors in the financial statements.

Qualified opinions: Financial statements have some material misstatements. There may also be failure to comply with legislation or the performance information can be faulty.

Adverse: The auditor disagrees with management on the financial statements as they have significant flaws and are not a fair reflection of the financial position, performance and cash flow.

Disclaimer: There is lack of sufficient and appropriate audit evidence to express an opinion.

Infographic:

Comments

Keep comments free of racism, sexism, homophobia and abusive language. People's Assembly reserves the right to delete and edit comments

(For newest comments first please choose 'Newest' from the 'Sort by' dropdown below.)